Finding reliable data on executive compensation in Germany is more difficult than it should be. The reason: Benchmark surveys usually summarize Europe in a single number.

If the surveys do provide specific evaluations for Germany, the data is based on a thin basis that is not suitable for deriving actions. This is because country-specific patterns are often lost when data are broken down to the country level. In addition, the structural peculiarities that characterize Germany – phantom shares, the lack of an enterprise management incentive equivalent (EMI equivalent) and regulatory changes – are rarely adequately explained. So what does the data show?

The base salary is competitive

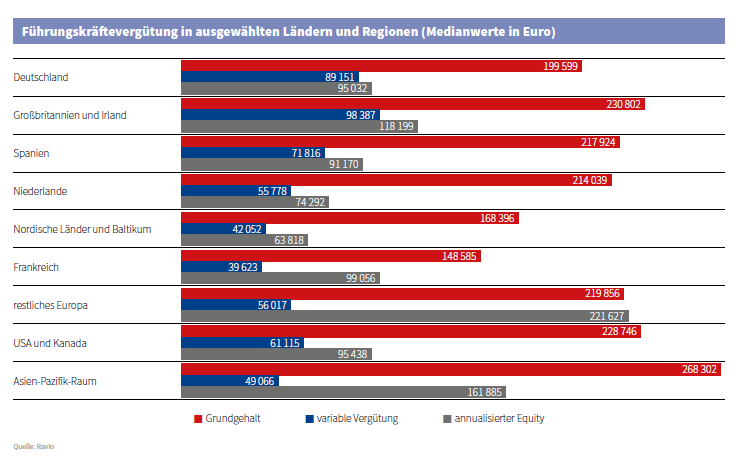

The average basic salary for managers in Germany is competitive, but not outstanding. It is around 200,000 euros. This puts Germany slightly below the Netherlands (214,000 euros), Spain (218,000 euros) and significantly below the United Kingdom and Ireland (231,000 euros). At first glance, this sounds like a pay cut for German executives. But the basic salary is only part of it. Once variable compensation and equity come into play, Germany’s position changes significantly.

Solidly positioned with variable remuneration

The median variable compensation for managers in Germany is around 89,000 euros. This exceeds the values in the Netherlands (56,000 euros) and Spain (72,000 euros), but is below those in the United Kingdom and Ireland (98,000 euros).

The pattern reflects the European trend: variable compensation increases as the company matures. At C level, i.e. the highest management level in the company, bonuses are predominantly linked to company performance. At the Vice President level, however, individual goals play a greater role. CEOs receive the highest variable shares, followed by sales and customer success executives.

In late-stage companies, it can be seen that variable compensation is declining – unlike in high-growth companies. This is a break with the European pattern. With increasing maturity and more formalized governance structures, equity takes on the incentive function that bonus payments fulfill in earlier phases.

Equity: the strongest German plus point

The median annualized equity of managers in Germany is around 95,000 euros, well above the Netherlands (74,000 euros), Spain (91,000 euros) and the United Kingdom and Ireland (118,000 euros). This one number changes the entire compensation picture: managers who accept a lower base salary in Germany receive the most generous equity packages in return.

Standard vesting conditions apply to the packages: 75 percent of the packages use a four-year vest, 65 percent are structured monthly. These principles are consistent across Europe. However, Germany differs in the type of equity it offers.

Phantom shares as a strong option

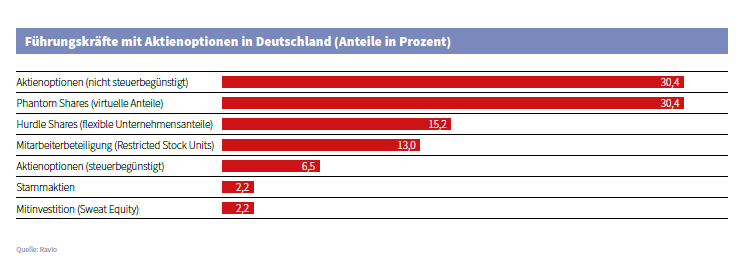

Around 60 percent of European executives receive stock options. In Germany this proportion is around 30 percent. Germany fills the gap primarily through phantom shares. There are structural reasons for this.

Germany has no direct equivalent to the British Enterprise Management Incentive Program, or EMI program for short. This offers significant tax advantages on stock options in early-stage companies. Since this mechanism does not exist in Germany, stock options are subject to double taxation in this country: on the one hand when they are converted into shares and on the other hand when they are sold.

The situation is different with phantom shares, i.e. contractual promises to pay out a cash value in the event of a liquidity event, without direct share ownership. These are only taxed once, namely on the liquidity event itself. For early-stage and high-growth companies, phantom shares reduce administrative effort and meet the expectations of German tech talent.

Therefore, reward executives designing equity programs should be guided by the German market and not adapt a structure developed for the UK or US. In the German context, a well-structured phantom share plan is often a strong offer.

Gender pay gap: need to catch up in Germany

The unadjusted gender pay gap in Germany is particularly significant at management level, especially when it comes to variable compensation and equity. The gap in Germany is larger than in the Netherlands and Great Britain and half as large as in France.

These figures are subject to the caveat of “unadjusted”. At the management level, the distribution of roles has a strong influence on the outcome of the gender pay gap, as CEO positions are disproportionately often held by men. This distorts the male median upwards. Comparisons, adjusted for role, function and company stage, are required before conclusions can be drawn.

However, the unadjusted figure shows where the focus should be: companies preparing for the reporting requirements of the EU Pay Transparency Directive will include equity and variable compensation at management level among the first areas examined. Getting a role-adjusted overview now is more valuable than waiting for the reporting requirements to come into force.

Three insights for Comp & Ben

The German market for executive compensation has three characteristics:

- The total compensation is more competitive than the base salary suggests. Executives who accept a lower base salary in Germany receive the highest equity packages in Europe.

- Phantom shares are not an exception, but the market standard. Compensation structures for German employees should be designed for the local market and not be an adaptation of a British or American template.

- Data on the adjusted gender pay gap should first be available before companies make political decisions. However, the unadjusted data at Equity is already sending a signal that the analysis should be carried out immediately – and that structural inequality should not be judged in advance.

Author

Alex Zietek,

Regional Marketing Manager,

Ravio

[email protected]

www.ravio.com

")